Broadstreet Bulletin issue 15

May you live in interesting times…

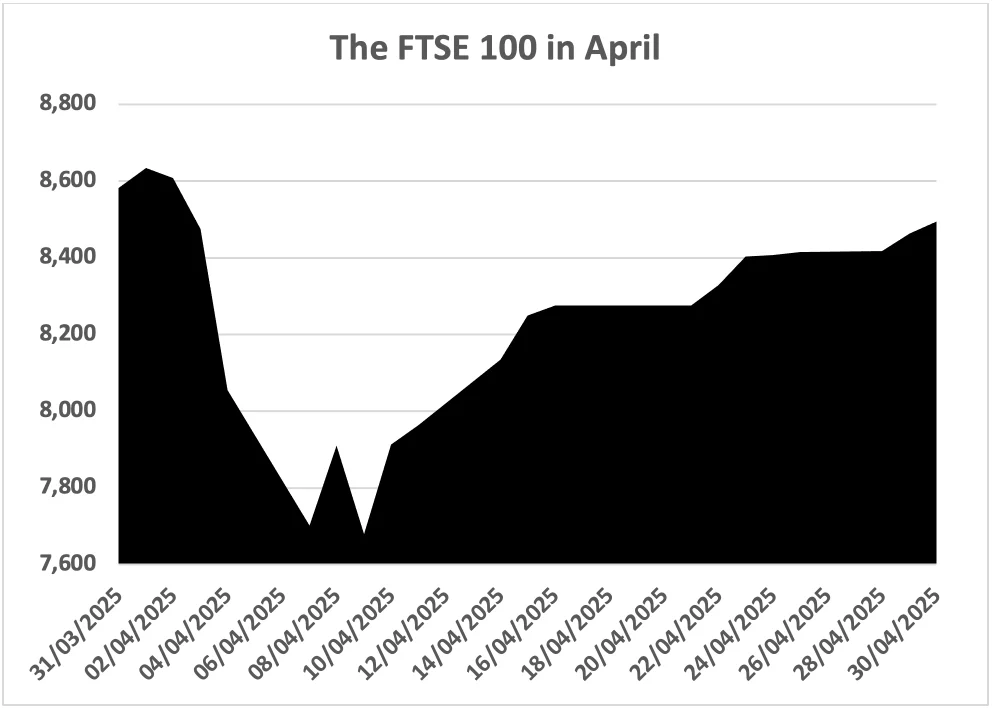

There are times when how you view investment performance can make a great deal of difference, even if the end-to-end results are identical. April 2025 provided a classic example, as the graph above shows all too clearly. From close of business on 31 March to close on 30 April, the FTSE 100 index registered a decline of just over 1% – a nothing-to-see-here month.

On a long-term graph which simply uses end of month FTSE 100 levels, the change would be barely noticeable – in the first four months of 2025 the Footsie was up 3.9%. With a short-term view using daily price levels, as the graph above does, the picture is very different – by 9 April the index had fallen 10.5% in just seven trading days, equivalent to 1.5% a day. A plot that drilled down further, to minute-by-minute index readings, would look even more dramatic.

The Donald effect

The volatile pattern of the FTSE 100 was echoed in most other global stock markets. For example, the S&P 500, the main US equity market index, fell over 11% between 31 March and 8 April. The day earlier timing for the peak fall stems from the main cause of the turbulence: Donald J Trump. His announcement of “Liberation Day” tariffs after the US stock market closed on 2 April was what prompted indices to dive. While investors had been anticipating that the President’s Rose Garden event would not be good news, the size of the proposed tariffs – and their arbitrary calculation – was totally unexpected.

A week later, on 9 April, Trump announced a 90-day pause in most of the tariffs (while maintaining a minimum 10% tariff and pushing China’s rate up to a blockade-type total of 145%). Probably deliberately, this news was released while the US markets were open. The S&P 500 leapt 9.5% with relief and other markets responded similarly on 10 April, as they opened. Once it was seen that Trump was willing to back down, despite all his rhetoric, markets steadily made their way back to around where they had begun the month.

Further tariff concessions have continued since 8 April, such as the UK trade ‘deal’ (which is not even a legally binding document) and US/China agreement to cut their mutual import levies by 115% for 90 days. The ongoing retreat from the “Liberation Day” onslaught took many markets back above their 2 April levels by mid-May. However, there is now a new countdown to 8 July, when the original 90-day pause ends, which might give markets more concerns as summer progresses.

Lessons

The volatility of markets in April was not unprecedented – think back a little over five years to the start of Covid – but it was a shock. It offered some useful reminders:

- Trying to time investment is next to impossible. The initial pace of the fall and the whiplash back did in theory offer the potential for a quick profit, but it is only visible with that most powerful of investment attributes, hindsight.

- Long-term investors can do worse than ignore the daily cacophony of ‘expert’ commentary on market movements. Remember, April was overall a flat month for most markets.

- Maintaining a cash reserve is always important. In April it would have meant that if you required capital, you would not have been forced to sell during what proved (so far) to be a temporary market dip.

- USA shares are a dominant part of many portfolios, simply because their value counts for 60%-70% of global stock market indices – a much larger proportion than the US share of the global economy.

The message is more one of inaction. Watching every market move, yet alone reacting to them, is not to be recommended on financial or health grounds.

The experience of the last few months warrants that familiar caveat, past performance is not necessarily a guide to the future – even with Donald Trump in the White House until 2029. If you are uncomfortable about what that might mean to your investments and want to adjust your portfolio to help reduce volatility, please talk to us.

Are you heading for retirement poverty?

In April the New State Pension increased by £9.05 (4.1%) a week to £230.25. Almost simultaneously, the National Living Wage (NLW) rose by 77p (6.7%) an hour to £12.21. That NLW rate equates to £427.35 for a 35-hour week, just short of £200 a week more than the State Pension. The gap between the two underlines the need for private provision to make retirement affordable.

Successive governments have made various efforts to encourage retirement savings, including generous tax reliefs on pension contributions and automatic enrolment in workplace pensions. However, recent research suggests there is still a long way to go before most of the current working population can look forward to a financially comfortable retirement.

A 15.3 million miss…

The recently published 21st annual retirement report from Scottish Widows in conjunction with Frontier Economics estimated that “15.3 million people today are at risk of retirement poverty”. The report’s definition of retirement poverty draws on calculations by the Pensions and Lifetime Savings Association (PLSA), which regularly calculates how much net annual income is required to support three different retirement living standards. The report uses the PLSA’s figures for 2023/24, updated for last year’s inflation – and, as such, are very similar to the PLSA’s recently published figures for 2024/25.

They are:

Minimum | Moderate | Comfortable | |

|---|---|---|---|

Definition | Covers all your needs, with some left over for fun | More financial security and flexibility | More financial freedom and some luxuries |

Single Person | £14,800 | £32,200 | £44,400 |

Couple | £23,100 | £44,400 | £60,800 |

These figures exclude housing costs and are for retirees living outside London. When the report talks of retirement poverty, it is referring to projected net retirement income below the minimum level figure.

Why are so many people at risk?

You could be forgiven for thinking that the combination of a state pension at nearly £12,000 a year plus automatic enrolment in workplace pensions should be enough to stave off retirement poverty, but it is not. The report highlights three groups of people who are the most likely to face a financial challenge when they stop work:

- Squeezed low to middle earners. In this category, the current way in which automatic enrolment operates is an issue. Anyone earning up to £10,000 a year is not automatically enrolled, although many will have the option to opt in. For those earning above £10,000, the minimum contribution is based on earnings above £6,240, a deduction which can be a significant proportion of overall pay for modest earners, especially for part-timers. The report found that people in their 30s earning between £20,000 and £35,000 were the mostly likely to contribute at the minimum.

There is legislation on the statute book which permits the government to cut or even eliminate the £6,240 exclusion quickly, but there is no indication it will be used any time soon. Any reduction would increase employers’ pension contributions and, after this year’s controversial National Insurance rise and the hike in the NLW, the government does not want to go there.

- Generation Z (typically categorised as people born between 1996 and 2010). Generation Z is finding early working life harder than their Gen X or baby boomer parents experienced. Other financial goals have made saving for a distant retirement a challenge for Gen Z. A quarter of people in their 20s put saving for emergency expenses as their priority. 13% are not able to set aside any savings according to the research. The report calculates that 42% of people in their 20s are at risk of poverty in retirement, with close to another quarter on course to afford only a minimum retirement lifestyle.

- The self-employed. The latest data from the Office for National Statistics shows that about 13% of the UK’s workforce – 4.4mn people – are self-employed. This category have never been included in automatic enrolment, an oversight which more than ever looks an error. The report says that just over half of the self-employed are in danger of being unable to meet their basic retirement needs. A quarter are on track to achieve only the minimum retirement lifestyle, while almost another quarter are not saving at all. These grim findings are not news, as other research over the years has shown poor projected outcomes for the self-employed.

The underlying message from the research is that retirement savings need to be higher – and not just amongst the three most at-risk categories.

To find out whether you are on target for a minimum, moderate, comfortable or impoverished retirement, ask us for a personalised calculation.

Starting with a ‘3’ again…

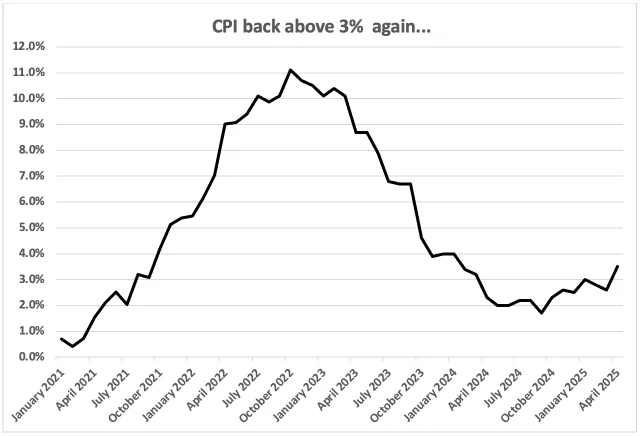

As the graph shows, inflation has been on a rollercoaster ride since the start of the decade. In August 2020, annual inflation as measured by the Consumer Prices Index was just 0.2%. A little over two years later, it was 11.1%.

That sharp upward spike surprised many economists, including those at the Bank of England. Throughout much of 2021 their assumption had been that price rises were, to use a now discredited term, “transitory”. It was not until December 2021 that the Bank increased its interest rate – from 0.1% to 0.25%. The rise marked the start of a series of interest rate increases which eventually ended In August 2023 with the Bank (Base) Rate peaking at 5.25%, where it remained for a year. By spring 2025 inflation had fallen back within the Bank’s target range (2%±1%), thanks to a mix of the high interest rate medicine and the unwinding of the COVID supply chain issues and Ukraine energy price distortions.

Successive governments have made various efforts to encourage retirement savings, including generous tax reliefs on pension contributions and automatic enrolment in workplace pensions. However, recent research suggests there is still a long way to go before most of the current working population can look forward to a financially comfortable retirement.

And then along came April…

April’s annual CPI inflation reading was 3.5%, an increase of 0.9% on March’s figure and the highest since January 2024. The Governor of the Bank of England, Andrew Bailey, had to write a mandatory letter to the Chancellor, explaining why the 1%-3% target inflation range had been missed and what the Bank was going to do to bring the rate back down.

The jump in April’s inflation figure was no surprise to practitioners of the dismal science (economics). April is a month when many price rises occur, such as the gas and electricity OFGEM cap, council tax, water rates and, increasingly, mobile and broadband charges. In 2025 there were additional inflationary pressures from the start of the higher employer National Insurance costs and the 6.7% increase in the NLW. The timing of Easter also played a part, pushing up air fares.

The utility bill rises were particularly problematic. In April 2024, the quarterly Ofgem cap fell by 12% to £1,690 a year, whereas this April it rose by 6.4% to £1,849 a year, making a year-on-year increase of 9.4%. Worse still were Ofwat’s water rate increases (which apply only to England and Wales). These marked the start of a new five-year cycle, but instead of spreading price rises over the half decade, the increase was heavily loaded to year one. Ofwat says the average water and sewerage bill has gone up by 26%, although there are significant regional variances.

Where next for inflation?

As the explanation above makes clear, April was an unusual month. However, those increases will stay in the annual inflation data until April next year, so there is not going to be a sudden summer reversal. The Bank of England is currently forecasting that inflation will peak in September 2025 at around 3.7% before gradually coming down to 2% by the first quarter of 2027. Other independent forecasters take a similar view – dare one say that the consensus is that the April 2025 inflationary jump will prove transitory?

A constant uncertainty

April’s 3.5% annual inflation is a reminder that the inflation dragon is never completely slain, despite the best efforts of the Bank of England and the many recent Chancellors. The dragon can lay dormant for long periods and then, as in 2021/22, suddenly – and ferociously – reignite. Even at lowly levels, inflation does damage – 2% inflation for ten years adds 21.9% to prices.

The corollary is that any medium or long financial planning, be it personal or business, needs to allow for inflation.

Check that your plans have not been left behind by inflation – to buy £100 of January 2020 goods and services on average now costs over £127

Do not let inflation erode your plans for retirement or family protection. If you think they need an update, find out now rather than when it is too late.

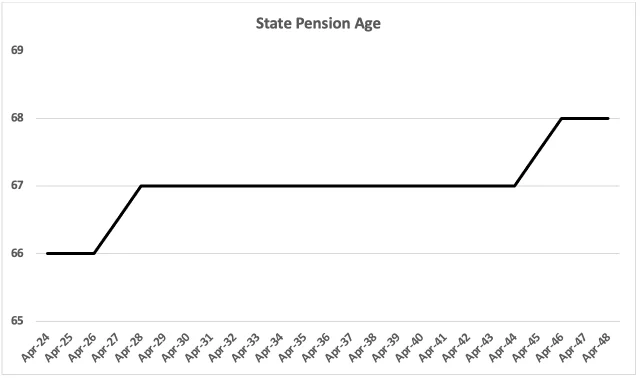

Less than a year away

On 6 April 2026, the next stage of State Pension Age (SPA) increases begins. If you were born after 5 April 1960, the move will affect you. The process will take two years, gradually raising the SPA until anyone born after 5 March 1961 will have to wait until at least age 67 to receive their State Pension payment (and stop paying National Insurance Contributions). The subsequent move to an SPA of 68 is currently due to begin in April 2044 (for those born after 5 April 1977), although this might be brought forward.

So, did you know?

If you were not fully aware of those SPA changes, you are not alone. Successive governments have struggled to communicate SPA changes, as was highlighted in the long-running battle waged by the WASPI women on SPA equalisation. Recent research undertaken by the Institute for Fiscal Studies (IFS) suggests the SPA message remains unheard by many.

The IFS used questions posed in a long-standing ageing survey between 2021 and 2023 about the SPA awareness of people born between 1955 and 1965 – those close to the transition from an SPA of 66 to 67. The results were:

- 60% knew their SPA accurately, which the IFS defined to be within three months. Unsurprisingly, those caught in the 2026-28 transitional period with an SPA defined in years and months were not as accurate as people with round number SPAs.

- 18% overestimated their SPA.

- 11% underestimated their SPA.

- 11% answered with the pollsters’ least favourite response, ‘Don’t know’.

SPA matters

The State Pension is a key part of retirement income for many. The IFS says that, for current pensioners, on average, it represents around 44% of total retirement income. Not knowing when that will start or, worse, expecting it to start earlier than the legislation dictates, could wreck your financial planning.

While previously announced SPAs can change, the government has said it will give at least ten years’ notice of an increase. After the WASPI experience, the pledge seems certain to be adhered to. The chances of the move to 68 being brought forward from 2044-46 now look limited, as life expectancy has not been improving as fast as previously estimated. If anything, the timing should be pushed back, but HM Treasury will probably have a view on that idea…

The underlying message from the research is that retirement savings need to be higher – and not just amongst the three most at-risk categories.

Do not let inflation erode your plans for retirement or family protection. If you think they need an update, find out now rather than when it is too late.

Your 2023/24 interest earnings

The prolonged period of near zero interest rates, which started in 2009 and lasted until 2022, meant that most savings accounts earned very little. Add to this the personal savings allowance (PSA – £1,000 for basic rate taxpayers and £500 for higher rate taxpayers) from April 2016 and having to pay tax on interest became almost a rarity.

And then rates started to rise…

The sharp upward march in interest rates throughout 2022 and 2023 changed the picture. Whereas a £30,000 deposit might have generated less than £300 before 2022, it could have produced £1,500 in 2023/24. Add in a freeze to the PSA and it was tax-free interest that became much scarcer.

Under current rules, normally, you do not need to complete a self-assessment tax return if your interest and other savings income is below £10,000. HMRC should still be aware of the interest paid to you, as it automatically receives the details from banks and building societies. In the past that information has allowed HMRC to collect tax via adjustments to your tax code, if you have earnings or a pension taxed under pay as you earn (PAYE).

For the 2023/24 tax year, when interest receipts jumped, HMRC’s system hit problems:

- HMRC faced so many interest computations that it did not finish them until March 2025, about five months after the formal deadline for taxpayers to register with HMRC.

- The HMRC mechanism for matching interest data to individual taxpayers is far from perfect. HMRC received 130 million automatic interest reports for 2023/24 and has been unable to link about 20% to taxpayer records.

Now what?

HMRC is now reminding taxpayers that the ultimate responsibility for calculating and paying tax due falls on the individual. It is advising anyone with a potential tax liability on their interest who has not received a HMRC interest tax calculation to contact HMRC as soon as possible to avoid a penalty.

If you have not heard from HMRC, check whether your 2023/24 (and, for that matter, 2024/25) interest was high enough to create a tax liability. If it was, do not delay in letting HMRC know.

If you are paying tax on interest, it may be that you are holding too much cash in reserve or missing opportunities to reduce your interest tax bill. Talk to us about your options.

Past performance is not a reliable guide to the future. The value of investments and the income from them can go down as well as up. The value of tax reliefs depend upon individual circumstances and tax rules may change. The FCA does not regulate tax advice. This newsletter is provided strictly for general consideration only and is based on our understanding of current law, the Finance Bill 2024/25 and HM Revenue & Customs practice as at 17 February 2025. No action must be taken or refrained from based on its contents alone. Accordingly, no responsibility can be assumed for any loss occasioned in connection with the content hereof and any such action or inaction. Professional advice is necessary for every case.

No comment yet, add your voice below!